Listed on

Don't have an account?

Register via AppHave an account?

Login

Don't have an account?

Register via AppHave an account?

Login

For all the talk of being in some sort of AI bubble, the idea that you can somehow pick the top in what is increasingly being described as a slow melt up can only be described as a “fool’s errand”.

We’ve seen more record highs for the likes the Dow, Nasdaq and S&P500 this week, along with the Nikkei 225, along with a modest softening of crude oil prices despite further kinetic skirmishes between the US and Iran.

Despite these skirmishes markets are increasingly becoming used to the idea that this is likely to be the status quo for quite some time now, and that in the absence of a full break down in negotiations, are able to take events in their stride.

While this might seem complacent it is becoming increasingly evident that investors appear to be focussing on the upcoming IPO of SpaceX, and what that might mean for the ongoing AI story, with this week’s numbers from Micron and Snowflake helping to underpin the bullish outlook further.

All eyes on Friday's US non-farm payrolls report for the latest read on jobs growth

__________________________________________________________________________________________________

This week’s US Q1 GDP revision while a modest downgrade to 1.6% has done little to change the view that the US economy remains resilient, with the upcoming May ADP and non-farm payrolls report expected to reinforce that idea.

The only concern for the US labour market has been the slowing participation rate which has been slowing for months now, and could be indicative of a wider structural problem.

We’ve also got some more earnings numbers from the Tech sector in the form of Broadcom and CrowdStrike, as well as the latest services PMIs from the UK and Europe which appear to be showing that rising input and energy costs are starting to weigh on economic activity.

Despite seeing a sharp 156k decline in February, the US jobs market has by and large looked resilient during 2026. Much of the reason for the decline in February was due to a strike by health care workers, along with cold winter weather which was reversed in the March numbers with a 185k gain. The strong March print was followed by a 115k gain in April, which showed that the US economy was showing stronger jobs growth than at the end of 2025. While the BLS numbers have proved to be erratic in recent months, other measures of job creation have proved to be steadier with the private sector ADP jobs reported showing consistent jobs gains since July last year, with the April ADP report of 109k showing the best number since January 2025.

Despite seeing a sharp 156k decline in February, the US jobs market has by and large looked resilient during 2026. Much of the reason for the decline in February was due to a strike by health care workers, along with cold winter weather which was reversed in the March numbers with a 185k gain. The strong March print was followed by a 115k gain in April, which showed that the US economy was showing stronger jobs growth than at the end of 2025. While the BLS numbers have proved to be erratic in recent months, other measures of job creation have proved to be steadier with the private sector ADP jobs reported showing consistent jobs gains since July last year, with the April ADP report of 109k showing the best number since January 2025.

Service sector PMI growth collapsed in May, falling to 47.9, down from 52.7 in April, and the sharpest downturn since early 2021. The main cause of this slowdown was a collapse in new orders, along with weaker investment sentiment. One factor, apart from the unrest in the Middle East was the increase in domestic political uncertainty which weighed on sentiment, along with further weakness in hiring trends. Combined with sharp increases in costs which have been driven by energy prices, higher government taxes/levies, along with wage costs and weak demand, the outlook for this sector has deteriorated sharply.

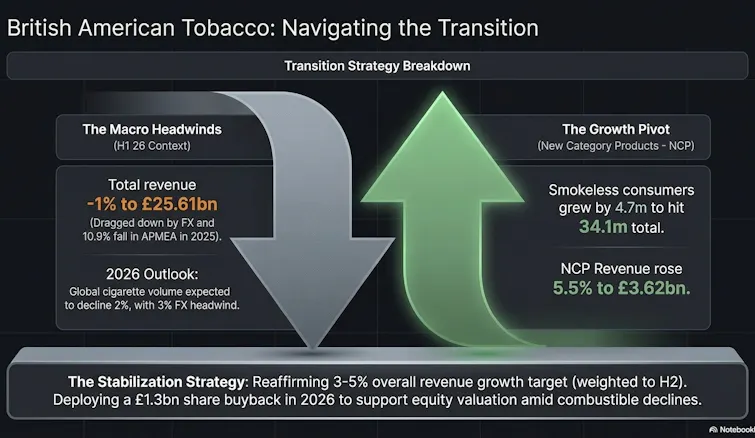

When British American Tobacco updated the market in February the company reaffirmed 3-5% revenue growth, 4-6% adjusted profit from operations growth, and 5-8% adjusted diluted earnings per share growth, weighted towards H2. At the end of its last fiscal year momentum for consumers of smokeless products grew 4.7m to 34.1m. Revenue for (NCP) new category products rose to £3.62bn, a gain of 5.5%, although total revenue still fell 1%, to £25.61bn due to currency headwinds. The company also announced a £1.3bn share buyback for 2026. The biggest drag on revenue in 2025 was down to a 10.9% fall in APMEA, while the US and AME saw an improvement in combustibles. For 2026 global cigarette industry volume is expected to decline by 2%, with a transactional FX headwind of 3%.

One of the lesser names in the AI story Broadcom shares have gone from strength to strength over the past 12 months, despite a modest setback in December when the shares fell sharply after their Q4 numbers prompted a sharp sell-off. Record Q4 revenues of $18bn, driven by a 74% increase in AI semiconductor revenue weren’t enough to prevent a 10% decline into year end, although some of this may well have been down to end of year profit taking. This weakness continued into March this year due to concerns over an AI bubble, before a rebound which has seen the shares return and surpass the previous record highs seen in December last year. For its Q1 numbers the company beat on expectations with a 29% increase in revenues of $19.3bn, helped by a 106% increase in AI semiconductor solutions of $8.4bn. This is where the main growth area of the business is, with the VMWare segment helping to deliver 1% growth in the infrastructure software segment. Capital returns were $10.9bn in Q1 with $3.1bn in dividends and $7.8bn in share buy backs. For Q2 the company said it expects to see revenues of $22bn.

In 2024 the name CrowdStrike became front page news after the company delivered a faulty update to its Falcon Sensor security software that caused widespread disruption to Microsoft Operating systems. This faulty update caused the crash of 8.5m systems in what was one of the largest global outages in the history of IT. The financial damage was huge, estimated at $5.4bn, as airlines, airports, hotels, manufacturing businesses, as well as banks, financial markets were all affected along with emergency services. While the error was fixed within hours, the after effects lasted days and the company’s share price tanked hard, halving in value in the space of weeks, although the company did manage to hold onto most of its customers in the aftermath.

While insurance payouts covered most of the costs, the reputational impact on CrowdStrike was sizeable with management working hard to restore it. Since then, the shares have managed to recover strongly, albeit in a volatile fashion with two more sharp sell-offs in 2025, which saw the shares lose a sizeable chunk of value, bottoming out at $343, in February this year, before rebounding to the new record highs we see today. At the end of Q4 the company reported a 23.6% increase in revenue to $1.31bn, with annual recurring revenue coming in at a record $5.25bn. The company’s subscription model Falcon Flex saw strong adoption, seeing 120% growth year on year, while client retention came in at a gross 97%. For Q1 2027, the company said it expects to deliver total revenue of between $1.36bn and $1.364bn, and net income of $275.2m and $277.1m. For the full year, total revenue expectations are for between $5.87bn and $5.93bn, and net income of between $1.24bn and $1.27bn.

Markets continued their steady climb higher this week, with major indices hitting fresh record highs as investors brushed aside geopolitical tensions and a modest downgrade to US GDP growth. The AI trade remains firmly intact, with attention turning to the upcoming SpaceX IPO and strong earnings from Broadcom and CrowdStrike keeping sentiment buoyant. On the macro side, the US jobs market looks stable ahead of Friday's non-farm payrolls report, though a declining participation rate is raising longer-term concerns. In the UK, a sharp contraction in the services PMI signals that rising costs and political uncertainty are beginning to bite.

1. Why do markets keep hitting record highs despite all the uncertainty?

Investors appear increasingly comfortable with the current backdrop, viewing geopolitical tensions as manageable and focusing instead on the strength of the AI investment story. With earnings from major tech names continuing to impress, the path of least resistance remains upward.

2. What is the SpaceX IPO and why does it matter?

SpaceX is the privately held rocket and satellite company founded by Elon Musk. Its anticipated IPO is being closely watched as a potential landmark moment for the AI and technology investment narrative, with many expecting it to attract significant investor interest and further fuel market enthusiasm.

3. Should I be worried about the US labour market?

On the surface, jobs growth remains steady and weekly jobless claims are low. However, the participation rate — the share of people either working or actively looking for work — has been quietly declining and is now at its lowest level since October 2021, which could point to a deeper structural shift worth monitoring.

4. What does the UK services PMI collapse mean for the economy?

A reading below 50 signals contraction, and May's drop to 47.9 suggests the UK services sector is under real pressure. Rising energy costs, higher taxes and weak demand are all squeezing businesses, and if the trend continues it could weigh on broader economic growth.

5. Why is Broadcom significant to the AI story?

Broadcom is a major supplier of AI semiconductors and networking chips that underpin the infrastructure powering AI development. Its Q1 AI revenue more than doubled year on year, making it one of the clearest indicators of how much money is being spent building out AI capacity globally.

The materials contained on this document should not in any way be construed, either explicitly or implicitly, directly or indirectly, as investment advice, recommendation or suggestion of an investment strategy with respect to a financial instrument, in any manner whatsoever. Any indication of past performance or simulated past performance included in this document is not a reliable indicator of future results. For the full disclaimer click here.

Join iFOREX to get an education package and start taking advantage of market opportunities.

A beginner's e-book

A beginner's e-book $5,000 practice demo account

$5,000 practice demo account A 12-part video course

A 12-part video course Trusted partner

Trusted partner

Featured partner

Featured partner